Texas Housing Insight

The Real Estate Center by:James P. Gaines, Luis B. Torres and Wayne Day (1-14-16)

The Texas economy continued to grow in November but at a more modest pace in the face of a weakening global economy, lower energy prices, and a strong dollar. Total employment expanded but was weighed down by the manufacturing and oil and gas extraction sectors, especially in Houston. Housing demand has started to show signs of slowing down in Texas while new construction was constrained by a shortage of skilled labor and developable lots.

Supply

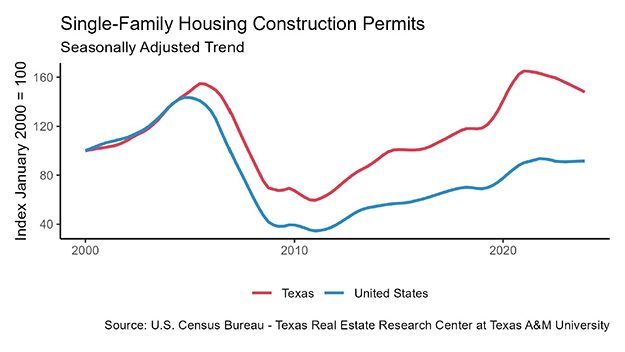

The Texas Residential Construction Leading Index (RCLI), which signals future directional changes in the residential construction business cycle of single- and multifamily housing, continued to increase in November. The RCLI was positively affected by increases in weighted building permits and especially by housing starts that registered a strong increase in the second half of 2015. Multifamily construction remained robust. The Texas Residential Business Cycle (Coincident) Index measures current construction activity; it turned down in November after a slowdown in activity during prior months. Single-family housing construction permits statewide increased moderately in November with declines in the year-over-year growth in Austin and Houston. Dallas continued with sustained growth though slowing down. No major MSA has reached its prior peak permitting levels. Housing starts in Texas continued to climb in November, helping alleviate the restricted supply somewhat.

Months of inventory for existing homes across Texas remained low but registered modest upticks the past couple of months to nearly 3.5 months of inventory (around 6.5 months of inventory is considered balanced). It is still too soon to tell if a trough has been reached, and an upward trend will continue going forward.

Demand

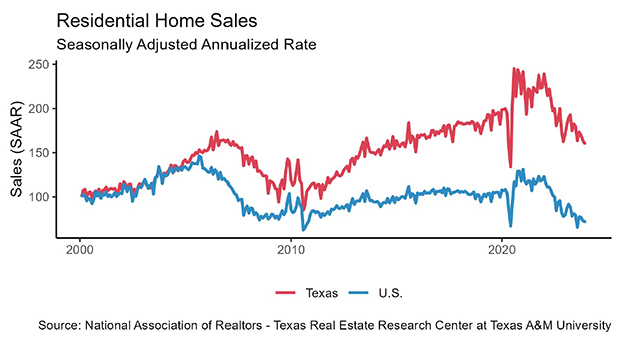

In November, total Texas housing sales decreased 0.5 percent year-over-year seasonally adjusted and decreased 1.8 percent on a not seasonally adjusted basis. Three of the five major metros — Austin, Dallas and Fort Worth — posted solid home sales increases. Houston had a negative 5.6 percent year-over-year seasonally adjusted change (negative 10.7 percent not seasonally adjusted). Year-to-date, 2015 Texas home sales registered positive growth, but the rate of change lagged behind the nation. Mortgage interest rates have remained slightly below 4 percent. In November, the Federal Home Loan Mortgage Corporation reported a 3.94 percent average rate on a 30-year, fixed-rate mortgage, while the 30-year U.S. Treasury bond yield equaled 3.03 percent.

The number of days an existing home was on the market remained low relative to prior periods reflecting the tight supply. New homes had somewhat longer November sales periods in Austin and Houston compared to Dallas and San Antonio. The average statewide difference to sell a new home versus an existing home was 39 days in November.

Prices

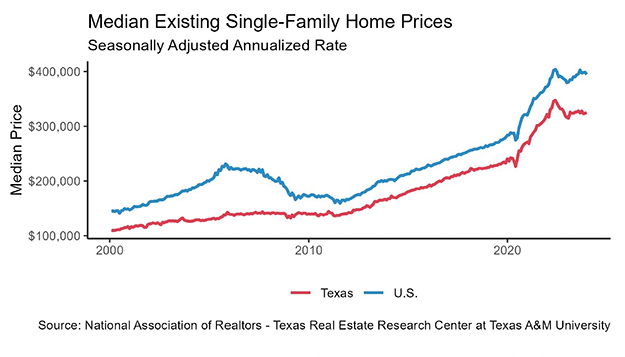

Average and median sales prices have risen dramatically in Texas since 2011 and continued to climb in November. The constrained supply, in conjunction with strong demand, accelerated price gains. Austin has been the house-price-appreciation leader through November 2015. Nonenergy employment growth and a strong services sector caused Dallas to register even stronger price appreciation, followed by Fort Worth and San Antonio. Due to recent declines in the energy sector and the resulting economic slowdown, Houston has begun to exhibit a softening in price growth.

Texas’ existing and new home sales prices have steadily climbed in the major metros. Since 2011, new median home prices exceed existing home prices by 48 percent and by 37 percent based on average sales prices. This price differential results primarily because of increases in home size for newer homes and the significant increases in construction and land costs for new homes. The price per square foot for a new home in Texas was almost 20 percent more than for an existing home.

Even with rapid price appreciation, purchasing a home in Texas continued to be relatively affordable compared to the rest of the United States, but the gap appears to be closing. The rate of increase in personal and household income greatly lags the increase in home prices.

Reply